Loans for older manufactured housing (how to buy a mobile home)

How to buy a mobile home: mortgage loans for older manufactured housing

This article resulted from a question asked by one of our readers. It turns out that many other visitors also wanted to know how to buy a mobile home. There are three issues that come up with buying mobile homes or financing older manufactured housing that don’t usually affect traditionally-built homes:

- Few real estate lenders will finance mobile homes built before 1976

- Manufactured housing must be taxed as real estate and placed on a proper foundation to qualify for a mortgage

- Mobile homes tend to depreciate like vehicles, not inc

rease like traditional housing - You might be able to finance a mobile home with a personal loan>>

The upside, though, is that you might be able to finance a mobile home if it’s residential real estate or personal property. There are companies that do both.

Following are rules and tips on how to get approved for manufactured home financing.

Verify your manufactured home mortgage eligibility here. (May 17th, 2019)

Financing manufactured housing as real estate

If your manufactured house is classified as real property, you may be able to finance it with a mortgage. Typically, it has to be built after 1976 (see explanation below). The loans work almost exactly the same as financing for traditional “stick-built” houses.

Most likely, you’ll get a Fannie Mae, Freddie Mac or government-backed mortgage. The VA, FHA and USDA all have manufactured home programs, but each has different rules.

You may need slightly higher down payments, slightly better credit scores, and/or pay higher fees. But these programs are still the most affordable financing for manufactured houses.

Verify your manufactured home buying or refinancing eligibility here. (May 17th, 2019)

Buying a movable (mobile) home

Houses you can hitch up and that you pay DMV fees for are movable homes, not real estate.

Manufactured housing loans for personal property — homes that are not classified as real estate — are readily available if you have at least five percent down and the home is reasonably new.

Interest rates are higher than mortgage rates because loans for movable property are riskier for lenders.

The FHA backs loans for mobile home vehicles with its Title I program. You negotiate your rate with private lenders offering this loan type. Note that these loans are offered by relatively few lenders and they prefer newer homes.

Personal Loans

You can also use a personal loan to finance a mobile home. Because a personal loan is based on you, not the property, there is no appraisal or questions about the home.

You might consider this option if your mobile home is too old or is missing its HUD tags or has other issues, you may be able to finance it with a personal loan. You likely need decent credit, and rates might be higher than a mortgage — but the lender won’t care how you spend the money.

Buy a mobile home even if it doesn’t conform to traditional mortgage standards, like being more than 400 square feet or it was built before 1976.

Maximum loan amounts are up to $50,000, but can be as high as $100,000. If you can’t get financing to buy your home, try a personal loan.

Verify Your Eligibility for a Personal Loan up to $100k*

*TheMortgageReports and/or our partners are currently unable to service the following states – CA, MA, NJ, NV, RI, WI

What’s with the 1976 cutoff?

Manufactured homes must have “HUD tags” to meet most mortgage lending guidelines. These tags, or more properly, certifications, state that the manufacturer complies with safety standards created by the Department of Housing and Urban Development, or HUD. A HUD tag ensures the home meets safety and livability standards, so it’s a good thing to have.

How to buy a manufactured home with a VA loan

This rule became law on June 15, 1976. HUD notes that while it is the only agency with this requirement, most lenders also follow its guidelines:

Prior to the 1976 rule, manufactured housing was prone to safety problems like electrical and wiring issues that caused home fires. Fireengineering.com states that “In mobile homes built before 1976, heating and cooking equipment are in close proximity to sleeping areas. This poses dangers to occupants and firefighters. The closer the source of the fire is to the sleeping area, the shorter the time the searching firefighter has to effect a rescue. Site-built homes have numerous areas in which to place utilities, and they usually don’t close the only escape route for occupants, as happens many times in mobile homes.”

According to the National Fire Protection Agency, “NFPA’s national fire data indicate that manufactured homes built to HUD standards (post-1976 construction) have a much lower risk of death if a fire occurs compared to pre-standard manufactured homes. ”

So the government created minimum safety requirements to protect buyers.

Why are mobile homes harder to finance?

One feature of mobile homes is obviously their mobility. So it is theoretically possible to take a huge residential loan on very favorable terms. Then you could hitch the new house up to your truck and drag it out of state or even out of the country. For this reason, lenders differentiate between manufactured homes as real estate and truly movable homes.

And that’s one reason that car loans usually come with shorter terms (five years, say, instead of 30) and higher interest rates. And that there is an entire industry built around recovering runaway autos.

In addition, most people expect their homes to increase in value as long as they own them, as long as they maintain the property. But manufactured houses tend to depreciate, or lose value, as they age. This also makes lenders less likely to approve loans for these homes.

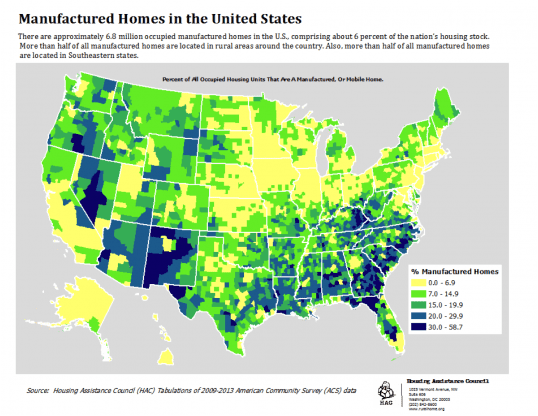

Source: Housing Assistance Council

However, in areas where more people own mobile homes, it’s probably easier to find financing. The darker areas in the map below indicate areas with a higher percentage of manufactured or mobile units.

How to buy and finance a manufactured or mobile home

When is a mobile home a house, and when it is a car?

To be a house and not a car, your manufactured home must pass a few tests, HUD says:

- The site must have permanent water and sewer hookup

- Facilities are approved by the local municipal authority, if

available at the site - An all-weather roadway must serve the site

- The entire property must be taxed as real estate

- The towing hitch or running gear must have been removed

- No part of the finished grade level under the home is below

the 100-year flood level - Structural integrity must have been maintained during

transportation and sufficient anchoring - Support and stability must be evident

These are not all criteria. Here’s a link to the whole set of guidelines. Alternatively, have an approved appraiser assess and value the property.

If you pay your annual taxes to the DMV, you definitely have a house. However, you can convert a manufactured home to real property by following the guidelines listed in the link above.

Financing an older manufactured home

Buying or refinancing a manufactured home can be tough. But look around for mortgage options like FHA, and non-mortgage solutions like personal loans.

To get a live rate quote for a mortgage, click the link below.

Verify your new rate (May 17th, 2019) Original Article Posted at : https://themortgagereports.com/37063/loans-for-older-manufactured-housing-how-to-buy-a-mobile-home