Loop Industries Inc’s “Independent Review” Of Its Technology Falls Flat

Hindenberg Research’s short report on Loop Industries Inc (NASDAQ:LOOP).

Q3 2020 hedge fund letters, conferences and more

- Two months ago we questioned Loop Industries Inc’s “revolutionary” process for recycling PET plastic that it claimed was “disrupting” the industry. Yesterday, Loop published an “independent review” that seems to indirectly confirm that its technology isn’t effective or economical.

- Loop claimed in its Q2 2020 SEC report that its new recycling process has “consistently high monomer yields, excellent purity, and improved conversion costs.”

- But Loop’s “independent review” of its process immediately admits that the verification “was not intended to certify the yields or economic viability of the technology of the process.” These omissions render the analysis largely meaningless.

- As a hypothetical to illustrate this point, what if a company pays $1 trillion to process a warehouse full of PET plastic to achieve an end product that’s “pure” but also the size of a dime? Information on purity without cost and yield is incomplete to the point of being irrelevant.

- A former Loop Industries Inc employee told us that without quantitative details on the process yield “the results mean nothing”. They pointed out that the testing left “a lot of room for interventions…from Loop’s team.”

- Our 30-year chemistry expert called Loop’s independent review “non-technical marketing material”, “very misleading” and concluded that “implying that [Loop’s process] is easy, inexpensive, and cost effective based on their released information is just wrong.”

- The review was run on four total batches of Loop’s process, yet data for several of these batches is reported with glaring inconsistencies or, in the case of one base chemical, incompletely reported.

- Buried in the exhibit of the 8-K filed Monday and not included in Loop’s press release was the review’s finding that “some operations” required “minor interventions” that would “have to be addressed at commercial scale”. With these issues arising at just a pilot scale, we believe an attempt at commercialization would prove to be a fruitless boondoggle.

- Our original report asked management 15 questions, ranging from why Loop’s initial funding was facilitated through a convicted stock felon to why the company’s two top scientists were in their 20s with no post-graduate education in sciences. Those questions all remain unanswered.

- It appears the market may have already started to figure out what we reveal in this report, as Loop stock has fallen precipitously since the company released the “independent review”.

- We remain short Loop Industries Inc’s stock with a price target of $0 and continue to strongly believe that Loop’s claimed technological advancements do not exist.

Loop Industries Inc Has Still Failed to Answer Any of Our 15 Questions and Instead Published an Analysis of Its Recycling Process Filled With Gaping Holes

On October 13, 2020, we released a report that challenged Loop Industries Inc’s claims of having a “revolutionary” process for recycling PET plastic. Our report cited multiple former employee whistleblowers, as well as industry experts, competitors and an extensive document review.

In addition to presenting our research, our report also asked management 15 questions, ranging from why the company’s initial funding was facilitated through a convicted stock felon to why the company’s two top scientists were in their 20s with no post-graduate education in sciences.

The company failed to address any of the questions we asked, but yesterday, 2 months later, Loop released an “independent review” of its recycling technology by research center Kemitek. Loop claimed the review confirmed the “effectiveness” of its technology.

To the contrary, the review appears to have validated our original findings, as we will show. We remain short Loop’s stock with a price target of $0 and continue to believe that Loop’s claimed technological advantages do not exist.

Loop’s “Independent Review” Immediately Admits It Does Not Focus on The Economic Viability Or The Yields Of The Company’s Technology, Rendering the Analysis Essentially Useless

As mentioned above, the company claimed as recently as October 7, 2020, to have a process that produces high yields and excellent purity at improving cost – what appears to be the holy grail of plastics recycling.

Loop Industries Inc’s Q2 2020 quarterly report spelled this out, describing the company’s new second generation process:

“Since June 2018, when we transitioned to this Generation II (“GEN II”) technology and our industrial pilot plant, we continue to see consistently high monomer yields, excellent purity, and improved conversion costs.”

Given the focus of our report and Loop’s claims about its GEN II process, we expected this “independent review” would attempt to affirm its prior claims about:

- The yield of the company’s process: Can the company quantify how much output is produced per unit of input? Determining how much is lost during the process is a key measure of efficiency.

- The purity of the finished monomers/base chemicals: Are there contaminants or inconsistencies in the “building blocks” that could prevent them from being put back together to make new sellable product (i.e., virgin PET resin)?

- The economic viability of the process: Can Loop’s process, at an industrial/commercial scale, make economic sense? Our first report asserted that Loop’s process is not economically viable – essentially the crux of its appeal to any investor.

Rather than getting answers to these 3 critical questions, the review instead presented this glaring disclaimer:

“The verification was not intended to certify the yields or economic viability of the process” [Pg. 3]

The “review” repeatedly commented on the purity of the end product without regard for yield and cost efficiency:

- “effective at producing pure monomers”

- “Kemitek’s findings through this verification allow us to attest to the capacity of Loop Industries Inc’s technology to produce pure monomers within their specifications”

- “Our findings through this verification allow us to attest to the capacity of Loop’s technology to produce pure monomers within their specifications.”

- “Independent testing by respected third-party research center confirms that Loop’s Gen II depolymerization technology is effective at producing pure monomers”.

As a hypothetical meant solely to illustrate this point, what if a company pays $1 trillion to process a warehouse full of PET to achieve an end product that’s “pure” but also the size of a dime? Such information on purity without cost and yield is incomplete to the point of being irrelevant.

Former Loop Employee: “No Yield, So The Results Mean Nothing”

30-Year Expert Chemist: The Review Amounts to “Non-Technical Marketing Information”

Again, purity, cost efficiency and yield together are important to substantiate the claims the company has made to investors in the past – and most importantly, the viability and economic potential of Loop Industries Inc’s process.

Upon review of Kemitek’s report, a former Loop employee told us that given the absence of yield “…the results mean nothing, especially as a viable technology for commercialization.”

The employee also told us that the 98.2% to 98.9% MEG purity in the review was “far from” the 99.9% MEG purity that was expected while they were at the company.

When we consulted a 30-year expert chemist about the supposedly scientific “review” they called it “non-technical marketing information”.

Former Loop Employee: Data In the Review Is Reported Inconsistently And/Or Incompletely, Suggesting The Company Is Having Difficulty at a Pilot Scale.

This Obviously Bodes Poorly For a Commercial Scale Operation (The Premise of Loop’s Existence)

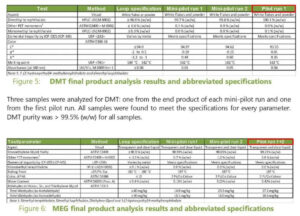

A former Loop Industries Inc employee pointed out that the review said Loop would run 4 batches total; two batches at each size (“mini-pilot” size and “pilot” size).

Yet, when the Kemitek reports its “Product Quality” specifications (figures 5 and 6), it shows only 3 runs for its DMT final product analysis (only one of the two pilot-sized runs is shown) and it combines pilot-sized runs one and two into one set of data for its MEG final product analysis.

This raised questions from the former employee, who suggested the data could be reported in this fashion to hide non-reproducible, potentially “very different” results.

This is not the first time we’ve seen selective data mining by Loop. In our original report, we pointed out a similar type of selective disclosure relating to one of its patent applications in which the company showed only one of the two resultant PET base chemical yields after distillation (MEG). [Pg. 22]

The failure in this latest review to report an entire pilot run and the combining of pilot runs suggests the results may be inconsistent and that the company is facing operational challenges at the pilot scale.

This obviously bodes poorly for a commercial scale operation, the apparent premise of the company’s existence.

Independent Review On Loop’s Process: “Some Operations Required Minor Interventions…Some Steps Would Take Longer Than Initially Planned”

Among the key issues raised in our original report was the question of whether or not Loop’s process can scale:

“Experts we spoke with raised serious questions about the company’s ability to make its “unparalleled purity” end product, as claimed, at large scales with any cost efficiency.”

Kemitek’s independent report noted that Loop Industries Inc’s process already needed minor “interventions” at the pilot scale and that these issues “would have to be addressed at commercial scale”. They attributed the issues to “either the size or design of the equipment”:

A former Loop employee who reviewed Kemitek’s report told us that this section indicates “they are not ready for industrialization and scale up to a production level.”

Former Loop Employee: Parameters Regarding “In-Person Surveillance” Of The Process “Leave A Lot Of Room For Interventions…From Loop’s Team”

A former Loop Industries Inc employee noted that the report’s comments about “In-Person Surveillance” of the process left “a lot of room for interventions on the process from LOOP’s team without Kemitek knowing about it”.

Specifically, we noticed one line that admitted it was “not possible” for someone from Kemitek to be in the production area 24/7 and additional color that seems to suggest Loop was on the honor system to consult Kemitek “before doing any intervention on the process”.

Contaminants In The Feedstock Used Were Not Quantified, Making It Difficult To Ascertain The Quality Of The Input Used For Testing

Quality of the feedstock (i.e., the “input”) plays a crucial role in the output of any final product in a chemical process. In the case of breaking down, purifying and reassembling PET, the more contaminated the feedstock, the more difficult it will be to create a purified end product.

Both our 30-year chemistry expert and a Loop Industries Inc former employee honed in on how Loop’s review appears to have not quantified exactly how contaminated its feedstock was:

“I don’t see how they would be able to quantify the components based on the information provided,” our chemistry expert told us. He also asked about the feedstock:

“While it was sent out to 3rd party and characterized, there are no results. The fact that there was ‘no tampering,’ so what? What were the results from the analysis?”

The only information about the feedstock was information that was obtained by internal testing at Loop, which we believe sullies its “independence”:

“The feedstock used throughout the verification consisted of pallets of post-consumer waste PET plastic. In appearance, it was a mix of clear, gray and colored flakes and fines with a PET content varying between 86% and 95%, as determined by a Loop-conducted analysis. Feedstock contaminants identified by external laboratories mandated by Kemitek include printed film, silicone elastomer and polystyrene.”

The former company employee also indicated to us that the feedstock used for the test may not have included items like rock and sand, which are common with PET and may have provided a more realistic test of the process.

30 Year Expert Chemist: Loop’s Review “Worded For Non-Technical People” And Is “Very Misleading”

Finally, our 30-year expert in chemistry characterized Kemitek’s review of Loop’s process as “very misleading” and told us:

“The issue is what is implied in their statements and conclusions reached in the testing that was ‘observed’ by Kemitek. It’s worded for non-technical people and very misleading.

Implying that [Loop’s process] is easy, inexpensive, and cost effective based on their released information is just wrong.”

Instead of Answering Our Questions, The Reviewer (Kemitek) Referred Questions Back to Loop.

Meanwhile, Loop Has Not Addressed A Single Question From Our Original Report

We reached out to Kemitek on December 14, 2020, with a list of several preliminary questions we had about their review. We asked about the amount, in grams, of PET used at the beginning and end of the process (which could help determine a yield) and whether the PET feedstock used was “typical” for post-consumer waste.

We were told by the Executive Director of Kemitek to “address all your questions to Loop as we are not mandated to respond to inquiries”.

Among other things, at the end of our report in October we listed 15 questions for Loop to answer. The company has since answered zero of these questions – so, we will list them again here:

- Was Daniel Solomita aware that Henry Lorin was a convict who had pled guilty to securities fraud charges when he was engaged to help raise early capital for Loop Industries Inc?

- If so, why did you hire a convict to help with your early capital raising efforts?

- Were you aware that Lance Bauerlein was under an active indictment for criminal securities fraud charges when you met with him to help facilitate Loop’s initial $80,000 investment?

- Did you expect that appointing two inexperienced individuals in their twenties with no post-graduate education in the sciences would yield a revolutionary breakthrough in the field of plastics recycling?

- According to several former employees, the R&D lab run by the Essaddams was producing results that couldn’t be replicated outside of their lab. How do you respond?

- Why does the company have two distinct labs? Is it best practice to limit access of the company’s scientists to a lab where major breakthroughs are said to be occurring?

- Loop Industries Inc’s competitors have published advancements and findings in scientific journals. Can Loop point us toward any relevant publications? If not, why has Loop not done this, despite all of the company’s claimed breakthroughs?

- When Loop claimed in 2017 that it was able to break down PET to its monomers at industrial grade purity, had MEG been consistently and successfully isolated at the time? Former employees state that it was mixed with dyes, water, and solid wastes. How do you respond?

- In 2016, Loop claimed to break down PET at a recovery rate of 100%. A polymer expert with over three decades of experience and former employees have described this recovery rate as “impossible”. How do you respond?

- Can you quantify exactly how much plastic Loop has recycled in conjunction with L’Oreal, Coca-Cola, and Danone since the announcement of these partnerships? Has there been any offtake from these companies, and if so, how much?

- Have L’Oreal, Coca-Cola, Pepsi, and Danone actually seen the entire Gen II process work from start to finish, using actual post-consumer waste PET?

- Why has it taken over 2 years to finalize terms of the joint venture with Indorama? Further, why did the company recently engage new partners instead of furthering its cooperation with Indorama?

- What is the status of the Drinkfinity partnership, given that the website doesn’t even appear to function?

- Why were Drinkfinity bags made with LDPE when Loop Industries Inc can’t recycle that plastic?

- We understand the company’s patents deal with depolymerization, but we also know these methods to be relatively well known already. Does the company have a patent on any specific purification methods that can be proven to purify PET monomers in way that exceeds the industry’s current best practices at an industrial scale?

Maybe one day investors will get a response.

Conclusion

It appears the market may have already started to figure out what we reveal in this report, as Loop Industries Inc stock has fallen precipitously since the company released its review.

As we stated in our original report, we continue to believe that Loop’s claimed technological advantages do not exist and that the company does not have the science to back up the claims it has made on its website, in its investor decks and in its SEC filings, since its inception as a public company.

Disclosure: We are short Loop Industries Inc (NASDAQ:LOOP)

Legal Disclaimer: Use of Hindenburg Research’s research is at your own risk. In no event should Hindenburg Research or any affiliated party be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. You should assume that as of the publication date of any short-biased report or letter, Hindenburg Research (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors has a short position in all stocks (and/or options of the stock) covered herein, and therefore stands to realize significant gains in the event that the price of any stock covered herein declines. Following publication of any report or letter, we intend to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation, conclusions, or opinions. This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Hindenburg Research is not registered as an investment advisor in the United States or have similar registration in any other jurisdiction. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Hindenburg Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and Hindenburg Research does not undertake to update or supplement this report or any of the information contained herein.

The post Loop Industries Inc’s “Independent Review” Of Its Technology Falls Flat appeared first on ValueWalk.

Original Article Posted at : https://www.valuewalk.com/2020/12/loop-industries-inc-independent-review/<\p>