Rowan Street Up 65% In 2020; On Value Investing In The 21st Century

Rowan Street Capital commentary for the year ended December 30, 2020, discussing their value investing approach to the 21st century.

if (typeof jQuery == ‘undefined’) { document.write(”); }

Q4 2020 hedge fund letters, conferences and more

Rowan Street Capital (RSC) Performance

Dear Partners,

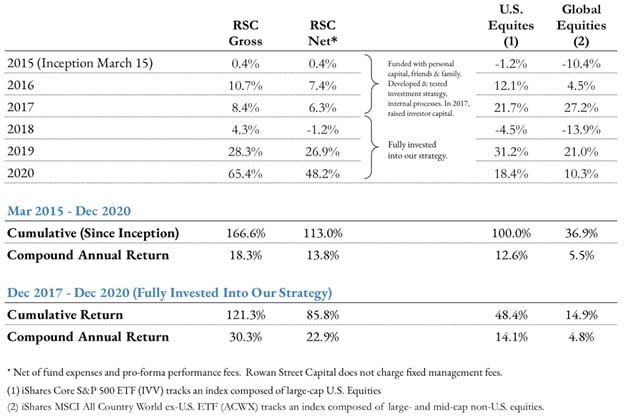

Rowan Street had a very successful 2020 — our best year since inception. Our fund recorded a return of +48.2% (net of fees and fund expenses), compared to +18.4% for the S&P 500 index. Since 2017 (fully invested period), our fund has returned +85.8% (net of fees) vs. +48.4% for the S&P 500. On an annualized basis, this equates to +22.9% per year vs. +14.1% for the S&P 500.

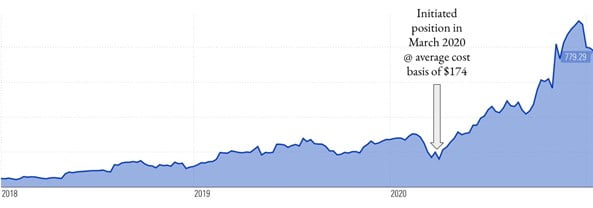

The biggest contributors to our outperformance in 2020 were Spotify (+110%) and Trade Desk (+355% since purchase). Spotify, we had purchased back in 2018 and had already outlined our investment thesis in our Q2 2020 letter. Trade Desk, we were fortunate to purchase in the midst of a market panic in March of 2020 (see below). Since we were fully invested at the time, we decided to trim our Facebook (FB) position to fund a small new position in TTD. This ended up being a very lucrative decision for the fund.

Another year of good news for our taxable investors!

Just like in 2019, almost all of our gains in 2020 were unrealized, which means that your Rowan Street tax bill for 2020 should be nominal. Compounding the fund’s capital while minimizing the checks that we write to Uncle Sam is our main objective.

The tax team at HC Global should begin working on the fund’s tax return shortly and will be sending your K-1’s later this spring when they are complete.

Expected Returns

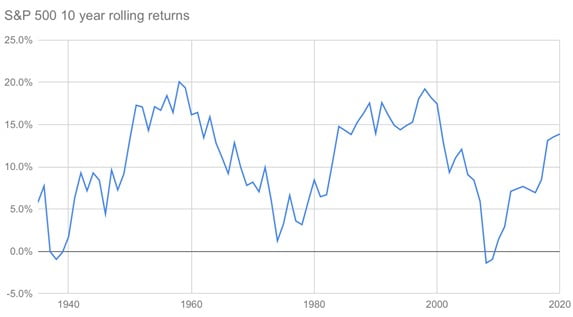

Below is a chart of rolling 10-year compounded returns for the S&P 500. At the end of 2020, the 10-year trailing market compounded return was approximately 14% per annum.

On average, the market has returned 8-9% per annum over time. Your total return comes from 3 components: Earnings Growth + Dividends + P/E Multiple expansion/contraction. Earnings growth for the S&P 500 has averaged at 6-7% per annum over time. Dividend yield has averaged at about 2-3% per annum. So roughly, over the past 10 years, the market’s 14% returns came from ~6% earnings growth + 3% dividend yield + multiple expansion (approximately 5% per annum). The reason we had such a tremendous multiple expansion since 2011 (unlikely to be repeated over the next 10 years) is the earnings multiples were extremely depressed at that time as the global economy was still in shambles from the Global Financial Crisis of 2008.

Now, every time the market experiences elevated (double-digit) returns over a 10-year period or longer, investors start developing very unrealistic expectations of future returns. This happened at the end of the 1990s, when the trailing 10-year market returns stood at extremely elevated 15-20% per annum, and naturally, investors were extrapolating their recent market experience into the future. As you can tell from the chart above, this proved to be very delusional. Similarly, today more and more market participants are expecting to get similar kinds of returns that the market offered over the past 10 years or so. We believe these expectations will also prove to be very delusional just like they did in the past.

A friend of mine, who runs an investment group on Facebook, which is made up of about 1,000 participants, recently did a poll of what type of returns people expect from their portfolios. I was shocked at the results. Majority expected to derive 15-20% annual returns; a good amount of people thought they could do 20-30%; only a small minority was humble enough to admit to a “very modest” 5-10% annual returns. As Warren Buffett once brilliantly put it: “Nothing sedates rationality like large doses of effortless money.”

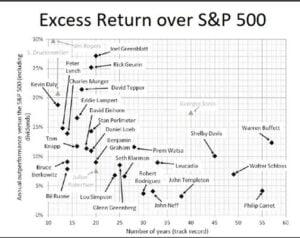

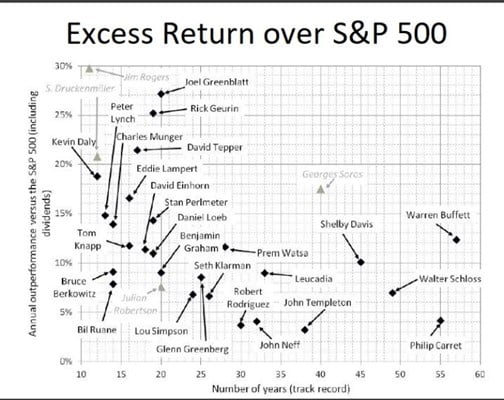

Now, let’s take a look at the returns the best investors of all-time have generated. Please refer to the chart below, which plots excess returns over S&P 500 on the Y-axis versus the number of compounding years on the X-axis. All of these guys are billionaires and anyone who can achieve a 5%+ excess return over an extensive period of time deserves to be a billionaire. We are mostly impressed with the longevity of the compounding track record (25+ yrs) of the very best. Warren Buffett has compounded at 20%+ per annum (~12% excess return over S&P 500) and has been in the game the longest for over 55 years. Walter Schloss (another all-time favorite of ours), who was also a disciple of Benjamin Graham, earned slightly above 5% excess returns and was in the game for almost 50 years — until he was 95 years old. Seems like the majority of that Facebook group that took the poll confidently place themselves in the same category as the all-time greats plotted in the chart below.

What can we expect from the Rowan portfolio over the long run?

By no means should you be expecting the fund to generate anywhere near the kind of returns that we had enjoyed over the past two years. These kinds of returns are unsustainable, and without a doubt we will experience a market decline (perhaps a significant one) at some point in the future. Some of our portfolio holdings may experience drawdowns of 50% or more from peak to trough, just like we did in March of 2020. This is normal and part of the game of long-term compounding. Remember, we are not in the game of minimizing volatility. We are not traders, hedgers, market timers or “renters of stock.” We are strictly business owners and compounders of capital! And just like Jeff Bezos, Reed Hastings, Mark Zuckerberg or Elon Musk have never sold when the stock of Amazon, Netflix, Facebook or Tesla had declined by 25% or 50%+, and have always focused exclusively on the long term fundamentals of their respective businesses, you should expect us to do the same with our portfolio companies.

We have no idea what the market is going to do over the next quarter or the next year, and we make no attempt to make such predictions. There is nothing in our record that suggests that we can add any value by making those predictions and trying to time the market, in contrast to an inordinate amount of energy and resources that is spent on these activities on Wall Street.

We remain focused on what we do well — identifying high quality, well-run businesses that are likely to compound our capital at double-digit rates of return over the long run, and we try to acquire those opportunistically when Mr. Market offers us an attractive price. This approach has proved to be successful for us throughout our investment careers and we will continue to focus on that because we think it’s logical, repeatable, simple and straightforward.

The Rowan Story

Joe and I had known each other for quite some time, first meeting many years at a CFA “boot camp” in Windsor, Canada. Both of us have had long professional careers on Wall Street, and have honed our investment philosophy and process for over a decade prior to starting our fund. In 2015, we finally decided to start Rowan Street out of frustration that we could not manage money for our clients the way we would do for ourselves.

Here is the truth that we discovered. Because of the inordinate amount of energy and resources within the world of professional money management focused on asset gathering, short term relative performance is an anathema because it precipitates client defection. At the risk of pointing out the obvious, if one is to perform better than average, one must, more than occasionally, stand apart from what others are doing. But this behavior invites periods of underperformance, which is disastrous to the retention of client assets. “Worldly wisdom teaches that it’s better for a reputation to fail conventionally than to succeed unconventionally” – Maynard Keynes. So the average money manager attempts to engineer a portfolio to retain clients and, of course, mediocrity is the result.

We believe that we could do better for our clients. The first two years of our existence, we stayed very small just working with our personal capital and that of our close friends and family. We set out to think and act like owners of businesses (rather than renters of stocks) and believed that we could achieve our long-term goal of double-digit compounding with enough patience and discipline, and of course, with like-minded limited partners that trust us and believe in our vision.

We were very cautious, methodical and not in any rush, initially only investing 25% of the fund’s capital while we tested our investment strategy and developed our internal processes that formed the foundation of how we run Rowan Street today. Our early results were satisfactory, as we achieved market-like returns in the 2015-16 period, even with the majority of our portfolio (~75%) sitting in cash.

In 2017, we found a significant number of new investment opportunities. This was a year that we were also lucky to raise a substantial amount of capital from new investors, and we spent the rest of the year deploying all that new cash into our newly found ideas. 2017 was also a huge pivotal year for us from an investment philosophy perspective.

Evolving Our Value Investing Approach to the 21st Century

In 2017, one of our limited partners and a good friend recommended a book: “Modern Monopolies: What It Takes to Dominate the 21st Century Economy.” I “swallowed” this book in about 2 days as I had been thinking about this topic for a few years at the time, realizing how network effects have created the strongest moats of the 21st century.

One of the biggest revelations for us that year was that in the past our thinking was heavily influenced by Warren Buffett and his 20th century success of finding businesses that are highly predictable and do not change very much. Observing the rapid technological advancements and the emergence of the platform companies in the 21st century that have had tremendous influence on our lives and are disrupting almost every single industry out there, had pushed us to evolve our value investing approach to the 21st century. We realized over and over again that, in fact, change is the driving force for creative destruction and value creation! Thus, we needed to spend more and more time understanding change and the people behind it rather than trying to find businesses that are unlikely to change over the next 5-10 years. This was a huge departure from what Warren Buffett (who we have an enormous respect for) was focusing on for the major part of his investment career and, what we believe, is the downfall of the majority of traditional value investors today who failed to come to this realization.

Portfolio Transitioning

2017 was a crucial year for us in terms of our mental revelation, but not in terms of the actual portfolio investments per se. All the platform companies that we were studying and wanted to own were having a great year: Alibaba (+96%), Facebook (+53%), Tencent (+115%), just to name a few. But our strict price discipline that insists on the Margin of Safety (a concept first developed by Benjamin Graham that also needed to be evolved to the 21st century) did not allow us to own these at the prices that Mr. Market was offering us at the time.

Finally, our patience paid off at the end of 2018, when both the Dow Jones Industrial Average and the S&P 500 had their second worst December on record (only behind December 1931 when the market lost 14.5%) as fear about the trade war, high interest rates and worries about slowing corporate earnings took over investors’ minds.

In our 2018 Year-End Letter we wrote:

Even though many were spooked by the market volatility in the fourth quarter, at Rowan Street we view volatility as our friend, not our enemy. In fact, assets can fluctuate greatly in price and not be risky as long as they are reasonably certain to deliver increased purchasing power over their holding period. We believe there is no wealth creation without volatility! It is simply the “price of admission” that the market demands you to pay, yet there is so much effort on Wall Street that is dedicated towards minimizing volatility. These efforts are catered towards nurturing clients’ emotional well-being while creating an illusion of safety, but almost always come at a huge cost of reducing clients’ long-term returns.

In the last three months of 2018, and especially in December, Mr. Market has finally given us an opportunity to own businesses that we had dreamed of owning at prices that presented us with some very attractive expected rates of returns. In fact, our internally calculated IRRs (Internal Rate of Return) for the next 3-5 years for these investments are in excess of 20% per annum. We used this difficult quarter to our advantage, and in our view, we entered 2019 with a significantly better quality of companies in our portfolio with much more favorable long-term prospects than we’ve ever had since the fund’s inception.

We love the following quote by Ben Graham because it’s so true: “We have seen much more money made and kept by ‘ordinary people’ who were temperamentally well suited for the investment process than by those who lacked this quality, even though they had extensive knowledge of finance, accounting and stock market lore.”

We believe that good investing is a whole lot about temperament, and it requires a weird combination of patience and aggression. One caveat, is you have to be self-aware of the boundaries of your own competencies. The opportunities that Mr. Market had presented us with at the end of 2018 and the aggression with which we acted to reposition our portfolio and to take advantage of those opportunities had set us up for the success that we experienced in the following two years, especially in 2020. Thus far, our actual market returns have matched up pretty closely with our expected IRRs we had written about (see above) in the 2018 Year-End letter.

Conclusion

As a reminder, the fund is open at the end of each month for new investments. If you would like to increase your investment in the fund, please reach out to Joe or myself. As always, we encourage you to refer new investors to join our expanding band of like-minded partners in our quest to compound capital at double-digit internal rates of return over a long-term investment horizon.

We want to thank you for your partnership. Joe and I have our entire net worths invested alongside you — we strongly believe in eating our own cooking. We are extremely lucky to be involved with such a great group of partners.

Best regards,

Alex and Joe

Appendix

For new investors in our fund, it is imperative that we write again (and again) about our distinctive governing principles that guide and define Rowan Street Capital’s investment and business decisions. They reflect our commitment and partnership with our clients.

Our Guiding Principles

At Rowan Street Capital we:

- Think like business owners: The overarching principle of our investment discipline is to approach buying a stock as though we were buying the whole business outright and retaining management.

- Think long-term: When making investment decisions we focus on the long-term prospects of the business and look beyond the short-term volatility and market unpredictability. We let volatility work to our advantage as we don’t believe volatility equates to risk. On average, individual stock prices fluctuate more than 75% in a 52-week period. We welcome volatility as volatile markets occasionally offer extraordinary opportunities.

- Think independently: We do our own original deep research and believe that independence of thought is key to long-term investment success. We also believe that relying on others’ analysis results in paralysis or panic under volatile conditions. Groups (groupthink) have a tendency to reinforce preconceptions and suppress critical thinking.

- Stay within our circle of competence: We only focus on businesses that we can thoroughly understand. We try not to fool ourselves and are not afraid to put an idea into a “too hard” pile.

- Stay curious and always keep learning: We have a curious mind and strongly believe that if we compound our knowledge every day and go to bed a little smarter than we were the night before, it will significantly add to our compounded returns over time.

- Always demand a margin of safety : When analyzing a business, we strive to be conservative and reasonable in our assumptions. We are disciplined investors, and purchase stocks only when favorably priced, which protects us from permanent loss of capital.

- Avoid leverage: We like to sleep well at night. Leverage can enhance returns, but it can also lead to huge losses of capital from which it can be impossible to recover. You can’t win a race if you don’t finish, and too much debt can take you out of the game at the worst possible time.

- Exercise patience and discipline to only invest in EXCEPTIONAL opportunities: There are no called strikes in investing, so we can wait patiently for the truly fat pitches right in our “sweet spot” before taking a swing. Once an exceptional opportunity is identified, we will make bold rather than timid decisions (meaningful bets) where we see high probability of above average returns.

- Do a lot of reading and thinking and NOT a lot acting: In that we are sort of the polar opposites to a lot of investors. Many investors do a lot of acting, and not a lot of thinking. We believe that activity is the enemy of returns, and we are quite comfortable doing nothing until there is something to do. “All of humanity’s problems stem from man’s inability to sit quietly in a room alone” – Blaise Pascal.

- Eat our own cooking: We believe in having a sizable portion of our net worth invested in our fund. We want our partners’ financial fortunes to move in lockstep with ours.

- Communicate with our investment partners as candidly as possible: Our guideline is to tell you the facts that we would want to know if our positions were reversed.

- Enjoy the journey: Mastery is not about perfection. It’s about a process, a journey. The master is one who stays on the path day after day, year after year.

.fb-background-color { background: !important; } .fb_iframe_widget_fluid_desktop iframe { width: 100% !important; }

(adsbygoogle = window.adsbygoogle || []).push({});

(function() { var sc = document.createElement(“script”); sc.type = “text/javascript”; sc.async = true;sc.src = “//mixi.media/data/js/95481.js”; sc.charset = “utf-8”;var s = document.getElementsByTagName(“script”)[0]; s.parentNode.insertBefore(sc, s); }());

The post Rowan Street Up 65% In 2020; On Value Investing In The 21st Century appeared first on ValueWalk.

Original Article Posted at : https://www.valuewalk.com/rowan-street-capital-letter-21st-century-value-investing/