Standard AVB Financial Corp (STND) – Very Strong Yield But Lacking Dividend Growth

We are always on the prowl for an undervalued, dividend growth stock in the community banking sector. The two of us love banks and enjoy diving into their financial statements to uncover these gems. In today’s dividend stock analysis, we will review a $1b bank headquartered in Monroeville, PA: Standard AVB Financial Corp, STND.

Financial Review of STND

Standard AVB Financial Corp. operates 17 branches/offices in Pennsylvania and Maryland. The bank has a strong dividend yield and payout ratio; however, the bank is lacking the long-term dividend growth history that usually is a prerequisite for a purchase for us in this sector. However, let’s open up some earnings releases and annual filings to take a deeper dive into the numbers!

STND released their fiscal year and fourth quarter earnings on January 30, 2020. The earnings release was short, sweet, and to the point, which makes it a very fun read for potential investors. The one thing that jumped out at me was the consistency of the results. Net income in 2019 was $8.8m, compared to $8.8m in 2018. Interest Income (aka top line revenue) followed a similar trend during the year. In 2019, their 12 month interest income was $37.7m, a slight increase compared to $36.8m in the prior year.

One line item that saw a significant increase in 2019 was their interest expense. Interest expense increased to $9.3m in 2019 from $7.5m. For a $1b bank with a Total Deposits balance of $734m, that is a large jump. So I want to take a deeper dive into that number. Unfortunately, the banks earnings release does not provide enough granular information to identify the cause of the interest expense increase.

See – Our Dividend Stock Portfolios, which include several community bank investments

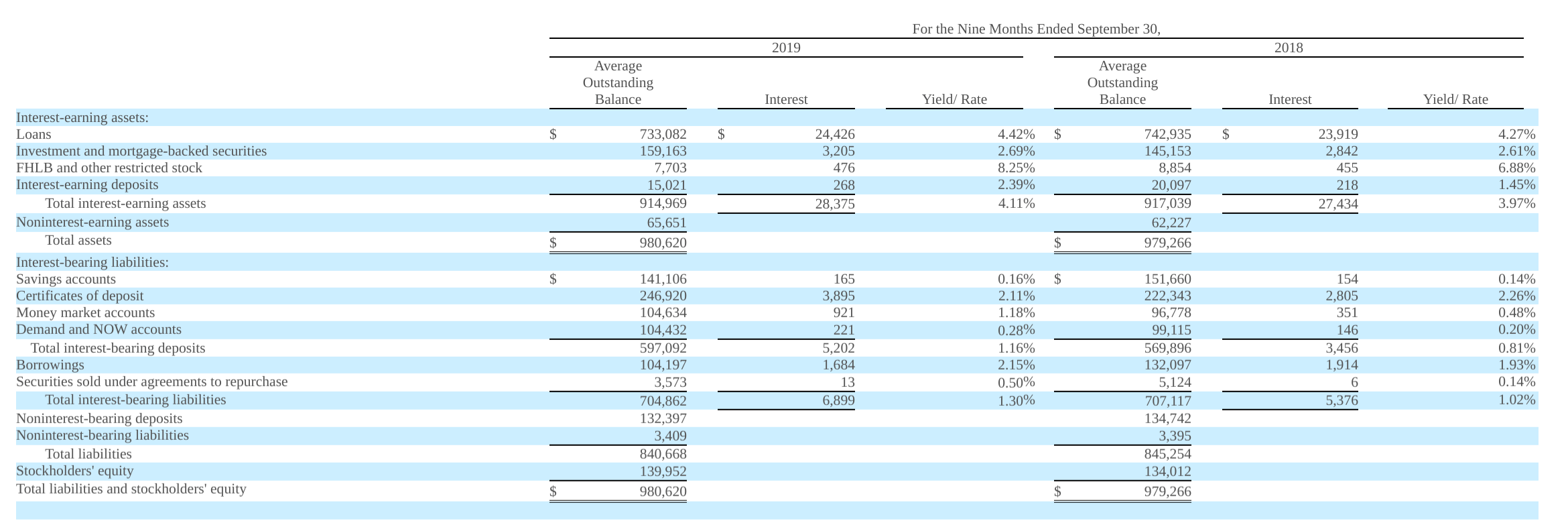

Since the bank’s 10-K has not been filed, I reviewed the bank’s 9/30/19 10-Q to see if the trend was evident. The table below shows the average balance of interest earning assets/liabilities, the interest earned/expensed, and the yield/rate of the line item. We will be able to learn specifics about the type of total deposit account and the average yield for the account as well.

The majority of the bank’s deposits are held in interest bearing deposit accounts. Of the four interest bearing deposit account types, the largest jump in the yield was in the money market account category. Not only did the average balance increase by ~$8m from 2018 to 2019, the average yield increase from .48% to 1.18% during the 12 month period. No wonder the bank’s overall interest expense increased so much during 2019.

Now, there is a change there will be some relief in 2020 for the bank’s overall deposit interest expense. Recently, the Fed announced an emergency rate cut in response to the horrible coronavirus pandemic. While interest rates increased slightly after the announcement, the Fed is expected to lower rates once again next week. So it doesn’t look like interest rates are going to be increasing anytime soon.

Since rates have decreased, banks have been slashing deposit rates to offset decrease in interest revenue. In particular, I have noticed rates on high-yield savings accounts, money market accounts, and other promotional type accounts were the first rates to be cut. This makes perfect sense to me. My gut tells me that the promotional rate that STND offered on their money market account will be slashed. I am expecting that yield to be much lower than 1.18% in 2020.

(adsbygoogle = window.adsbygoogle || []).push({}); Dividend Diplomats’ Dividend Stock Screener – STND

Now that we have reviewed STND’s recent financials, it is time to run the bank through our stock screener. The Dividend Diplomats’ Dividend Stock Screener examines the following metrics and is what we use to determine whether a company is considered an undervalued dividend growth stock.

- P/E Ratio (Valuation)

- Dividend Payout Ratio (Safety)

- Dividend Growth Rate and History (Longevity)

For this analysis, in order for me to consider investing in this bank, I want to see a payout ratio below 60%, a price-to-earnings (P/E) ratio below 13X (lower due to historically lower P/E ratios in the industry and the bank’s performance discussed earlier), and a dividend growth rate of 6.00% (given strength in desired yield). For dividend yield, we like to see community banks with a dividend yield above 4%. Let’s dive into the analysis.

Price-to-Earnings (P/E) – The bank has a P/E ratio of 9.53X. That is significantly lower than both the market and the threshold we set forth above. Further, we have reviewed community banks recently and noticed P/E ratios between 11X-13X. Of course, that was before the Coronavirus outbreak. So the industries range has definitely shifted downward.

Payout Ratio – We use a 60% target payout ratio in our analysis, as we believe 60% provides a strong blend of yield and the ability to continue growing its dividend going forward. STND’s dividend payout ratio is 46.53%. This is the perfect amount. I like to see payout ratios between 40%-60% because it indicates that management doesn’t pay too small of a dividend. This range also allows management to increase the dividend in the future without sacrificing its safety. A nice pass here for STND.

Read – What is the Dividend Payout Ratio? Learn how to calculate and analyze it here!

Dividend Growth History and Rate – This is where things get interesting for STND. Because STND does not pass either aspects here. First, the company has not increased their dividend since 2017. So their recent dividend growth rates is “N/A.”

Second, the bank doesn’t have a long-term dividend growth history. STND paid their first dividend in 2011. This short-term dividend history is troubling for a few reasons. Since their dividend wasn’t paid until after the financial crisis, I can’t tell how the company acted when times were tough. For most banks, I can see if they were able to grow, maintain, or had to cut, their dividend during the financial crisis. But starting in 2011 and on, things were relatively great in the banking community. Strong capital, healthy balance sheets, and so on. Next, their short term history doesn’t allow me to see if their lack of dividend growth was an anomaly or standard practice for the bank.

Due to their lack of recent dividend growth and their short-term history of paying a dividend, STND does not pass this metric of the stock screener.

Dividend Yield – The bank’s current dividend yield is 4.88%. Well above our 4% threshold.

(adsbygoogle = window.adsbygoogle || []).push({}); Summary

Overall, I like the bank’s consistent net income and interest income. Further, from a valuation standpoint, STND is trading at a discount compared to the market and other community banks. From a dividend perspective, their dividend yield is solid and their payout ratio is right in our sweet spot (40%-60%). However, the bank’s lack of a long term dividend history, along with the fact the bank has not increased their dividend since 2017, is a tough hurdle for me to jump over. I am a dividend growth investor that looks to find undervalued dividend growth stocks with a long history of increasing their dividend. With some of the dividend cuts that have been occurring in other industries (Occidental Petroleum, Delta, Boeing), I want to make sure I am focusing on companies that have consistently increased their dividend for a long time for my future investment decisions.

What do you think of my analysis? Would you invest in STND based on their current yield despite their long term dividend history?

Bert

The post Standard AVB Financial Corp (STND) – Very Strong Yield But Lacking Dividend Growth appeared first on Dividend Diplomats.