Vltava Fund 2Q20 Letter: The Dam Has Broken

Vltava Fund letter to investors for the second quarter ended June 30, 2020, titled, ‘The Dam Has Broken’, discussing the harmfull effects of negative interest rates.

if (typeof jQuery == ‘undefined’) { document.write(”); }

Q2 2020 hedge fund letters, conferences and more

If you are interested mainly in how our companies are getting on in the recession, you can jump straight away to the second part of this letter. I nevertheless would recommend you come back afterwards to the beginning of the letter, which is dedicated to a more general view on current goings-on in the markets.

Ideological Revolution

I don’t really care much for using grandiose words, because they often are spoken under emotional pressure and may prove exaggerated with hindsight. This time, however, they seem to fit the occasion. In my opinion, what we are living through just now is a time of ideological revolution insofar as monetary and fiscal policies of the world’s key countries are concerned. There are some things that one might perhaps have believed heretofore to be temporary but that will apparently become permanent aspects of the financial world while having great long-term impacts on the values of the main asset classes. Although for investors there is no escape, there nevertheless does exist a defence.

How Did We Get Here?

If I were writing some kind of academic text, I would have to start much further back in history. I think that for our purpose it is quite enough to start with the last recession in 2008. Its epicentre was in the financial sector. At that time, the central banks came up with a rather innovative solution that involved two main steps: purchasing assets from bank portfolios and reducing interest rates to historically low levels. Their combined effect was very positive, and particularly so in the first few years. They provided liquidity to the markets, brought stability to the financial sector, and spurred economic growth. This did not come for free, of course. Part of the private sector debt was transferred to governments, and their debts grew substantially. The balance sheets of central banks swelled to unprecedented levels while artificially low interest rates distorted prices in financial markets and created the temptation to underestimate risk. Central bankers answered to their critics with the argument that these were only temporary measures, and as soon as the situation in the markets would normalise the central banks would begin to reduce their balance sheets again and interest rates would go back to normal, too. This never happened, however, and it probably never will.

The Fed’s balance sheet, which expanded from USD 900 billion in the autumn of 2008 to USD 4.5 trillion at the end of 2014, started to contract slowly from 2018. But this only lasted for a year and a half, until autumn 2019, when it totalled USD 3.7 trillion. Then, practically overnight, the Fed made an unexpected 180-degree turn and began once again to purchase treasury bonds. It turned out, in fact, that there were not enough buyers in the market who would soak up the newly issued sovereign debt. Foreign investors have not been buying American debt very much in the past five years, and capacity of domestic buyers is not unlimited either. Last year, however, the country ran a deficit of about USD 1 trillion, and this new debt had to be bought up by somebody. The only remaining buyer was the Fed. By February 2020 (and that was still before the virus pandemic), the Fed’s balance sheet had bloated to USD 4.20 trillion.

Then came the virus, and this year’s US budget deficit will be not USD 1 trillion but rather USD 4 trillion, and if there were not enough buyers for the new debt already last year, that is even more so the case this year. The Fed’s balance sheet hit USD 7.00 trillion at the end of June and is still growing. Practically all new debt is now being purchased by the Fed. I am using the USA here as an example, but the situation is similar in all the world’s key economies – in the large countries of the EU, in Britain, Japan, as well as in China. This is a global problem.

What To Do About The Debt?

There are only three possibilities for settling sovereign debt. The first and best one is rapid economic growth. If an economy grows fast enough and is not burdened by a too-large debt, that debt may decrease as a percentage of GDP. For most of the big countries, however, this solution is outside the realm of reality. Their combination of slow growth and large debt practically excludes this, regardless of what politicians and central banks might say.

The second way of reducing the debt is to cancel it. This is a very common way of resolving the issue, and some countries having their own currencies will continue to use it. The latest big such case is the recent default by Argentina. This, however, is quite a drastic solution that is accompanied by great costs and difficulties and is politically unpopular.

The third way to diminish the debt is to let inflation wipe it away or, generally speaking, to repay it in depreciated currency. History knows many such examples dating back to Ancient Rome. This is and will remain the preferred manner of resolving debts in many high debt countries having their own currencies. This is nothing new, but the extent to which this solution is applied will probably accelerate.

The Dam Has Broken

National budgets are in the hands of politicians. If we take a cynical point of view (or maybe not even a cynical but a realistic one), we can say that the main interest of politicians is to be re-elected. The best path to winning election leads through bribing voters using state budget outlays. There is one unpleasant complication associated with this, and that is that if we want to give something to somebody we must first take it from somebody else. People are pleased to receive things, but they tend to get defensive when we want to take something away from them. What is happening now, however, changes the situation completely. Politicians see that it is possible to scatter money around without the need to take it from somebody else first, because the entire debt is financed by having the central banks print new money. This is nirvana to them. Now, they will shed even the last of their scruples. The result will be that large budget deficits will be predominantly financed by printing new money. “Helicopter money” is here in full strength. The dam has broken, and there is nothing that could stop the flood of new money.

In everyday life, scarcely anybody will raise objections against this. When you boost taxes on people, when they lose their jobs or when debts are cancelled, they protest. They are happy, however, when newly printed money is given away to them. They see only their own immediate benefit. The costs of this entire operation are too distant, abstract, and incomprehensible for them to recognise. It would be naïve, however, to think that these costs do not exist.

The whole thing works thusly: The government runs up large debt over the long term, the debt is underwritten by the central bank, and interest rates paid to the central bank by the government are returned by the central bank to the budget. Who would have any motivation to change this state of affairs? Reductio ad absurdum, the question arises as to whether it makes any sense to collect taxes at all when all the expenses may be paid by printing new money? I think it will not be too long before somebody comes up with this perpetual-motion machine.

And What About The Economy?

I have ever greater difficulties with economic theories. When I began enthusiastically to study economics in 1991, I considered it to be a science. Today, I seriously doubt that. An exact natural science for me is physics, for instance. When we reduce water’s temperature towards zero and below, we know what happens with water. It changes its state, volume, and other characteristics. It works the same every time and we all can agree on that. When we decrease interest rates towards zero and below, however, we do not know what will happen. Some economists consider negative interest rates to be very beneficial, some consider it very harmful. There is probably no real proof for either one. So, how can economics be a science?

Economics is right about one thing, though. The saying “There ain’t no such thing as a free lunch” declares that it is not possible to get something for nothing. Financing debt by printing new money truly has its real costs. They may be various – social, political, relating to ownership rights, and so forth. We are most interested in those that may involve financial markets.

The key to further investment considerations in my opinion comes down to two things. First, financing budget deficits by printing new money is now a permanent state of affairs. Second, a great part of this money will go directly to consumers because of the purposes for which the budget deficits are run, and over time this may have a considerable inflationary effect. It used to be that central banks were buying financial assets from institutional market participants, but today, a large part of newly printed money is directed to financing everyday outlays.

How Might This Influence The Markets?

It is thus probable that we will continue to invest in an environment accompanied by negative real interest rates, with nominal interest rates held artificially low, fiscal expansion, rapidly growing money supply, and inflating of central bank balance sheets. There does not occur to me any way how this may greatly change for the better any time soon. We’ve been working in this environment for some time already, but investors should change their thinking in the sense that this environment is not temporary but permanent. This whole trend will tend to accelerate with the speed of change in politicians’ and central bankers’ thinking. I believe it is no exaggeration to speak of an ideological revolution in finance.

Negative Interest Rates – The Greatest Threat To Investors

All the worlds’ main currencies have nearly flawless history insofar as their own depreciation is concerned. This trend will very probably even accelerate, and that is the main problem investors need to contend with. When I speak about currency depreciation, I do not mean exchange rates of currencies against one another. This is not a debate about whether it is better to own dollars, euro, pounds or francs. This is a discussion about the fact that all currencies lose value in relation to real assets.

Holding cash has historically been a bad investment choice because its real value is always sinking. Today the situation is even a bit worse, and holding a great part of one’s assets in cash over the long term makes practically no sense. And it may get even worse. Some economists are very seriously recommending to introduce substantially negative interest rates – to start with on the level of −3%. (From the future speech of the Great Economist to the nation: “Dear ordinary people, it gives me great joy to announce that from tomorrow we are introducing negative interest rates in the amount of 3%. Our economic theory clearly demonstrates that this step will bring you enormous benefit. It is true that we will take 3% of your savings each year, but do not forget the most important thing – that at least something will still remain for you. After 20 years, it still will be a bit more than a half.”)

It is a bit depressing to think that a person can work, earn money, and then instead of having and enjoying that money in peace, he or she has to continue investing just to protect the value of the money he had earned. This necessity is becoming ever more urgent even as there are fewer investment opportunities. The majority of debt assets are today essentially out of the game. Their real returns are either very low or they are inadequate relative to the credit risk taken on.

Essentially, the only way of preserving at least the real value of money over the long term remains ownership assets, and particularly shares in companies. Ownership of company shares (stock) should continuously bring greater returns than other investments, and that is for two main reasons: Shares represent the creation of value by human work, and there is opportunity to reinvest capital at higher rates of return.

I perceive every company as a living organism wherein people endeavour to create value by their work – contributing their ideas, efforts, creativity and common everyday labours. It may not succeed every time, but, on average and over the long term, this influence is very positive and, most of all, it is not eroded by the decreasing value of money.

Just about everybody will recognise, for instance, that the influence of Jeff Bezos on the value of Amazon is huge. The same could be said about the influence of Steve Jobs on the value of Apple. Both of them, together with other people in these companies, contributed crucially to the fact that the value of each of these companies exceeds USD 1 trillion today. We need not go so far to find examples of creating value by human work. Great creators of value in our Czech homeland, for example, were Tomáš Baťa, Emil Škoda, František Křižík and Emil Kolben. The names of great Czech value creators from the present need not be mentioned here, we all know them, even though in fact only one of these companies (Avast) is today publicly traded. It is one of the best examples of how people create value. Initially, the main creators of value were probably its founders Pavel Baudiš and Eduard Kučera, today they are almost two thousand employees.

People are simply the main instigators of value in a company, and so it is at all levels. These need not be gigantic corporations, either, not at all. People create value also on a smaller scale, in small firms, services and trade, for example. Every one of us either knows these examples from our own surroundings or is striving to do it himself or herself.

The influence of human activity on the value of a company is absolutely fundamental. People cannot by their work influence the value of other asset classes, like cash or gold or bonds, or they may be limited by the possibilities offered by such assets, as in the case of land or real estate, for example. In the case of companies, they have the greatest room, flexibility, and largest opportunity to adapt to changing conditions. This is the first and main reason why ownership of shares brings – and over the long term must bring – higher returns than can ownership of other asset classes. Nothing should change this in the future.

The second main reason why ownership of stocks should bring greater returns than ownership of other asset classes lies in the higher returns obtained from reinvestment of earned capital. Companies function over the long term by striving to reinvest earned capital into further growth and expansion. Reinvested capital increases the total sum of capital a company has at its disposal for doing business, and this should also bring increase in absolute returns. Capital reinvestment is of course possible also in cases of owning bonds, land or real estate, but in the case of companies the returns are much higher and the opportunities broader. For example, the average return on equity in the case of American publicly traded companies is around 12%. The companies may, on average, reinvest their own earned capital for that same rate of return. We scarcely can expect to attain such high returns when reinvesting into bonds, land or real estate. In long-term investing, when it is important how quickly the compounding returns accumulate, the difference between reinvested returns from stocks and reinvested returns from other asset classes is decisive.

None of these ideas is new or surprising. What has changed is the environment within which we invest. Some barriers that have existed up to now have been broken, and the degree of urgency to direct investments into ownership assets has increased. If you were to ask me if I like the hand that has been dealt, I would be very critical of many things and developments, but this has no influence on our investing. It is not important whether or not we like how things are developing. It is necessary to take things as they are, accommodate to them, and think about which stocks will benefit most in such an environment.

Changes In The Portfolio

In my last letter, I endeavoured to parse out how in my opinion the current recession may influence the value of companies in the Vltava Fund portfolio. So, how do things look like today, three months hence?

It seems that we were too optimistic in the case of WH Smith. Most of its stores were closed for some time. WH Smith therefore had to raise capital by issuing new stock. This will enable the company to get through the worst period, but the combination of the loss it will incur in this half-year, slower return to normal sales, and a greater number of shares in circulation means the fundamental value is lower than what we were contemplating at the end of March.

On the other hand, some companies in our portfolio are meanwhile faring better than we expected. Specifically, that is the case for Magna, BMW, Samsung and Humana. Magna is showing itself to be more resistant to recession than we had counted upon. Its operating leverage is lower than in the last recession, its balance sheet is strong, and it very probably will boost its market share during this recession, whether organically or by acquisitions.

BMW, meanwhile, is the only large car manufacturer to remain profitable, pay out its dividend in the originally intended amount, and not need to fall back on using credit lines from banks. Samsung recorded a drop in mobile phone sales, which was to be expected. On the other hand, its main and most profitable segment, which is producing semiconductors and memory devices, is doing better than we anticipated. This may in part be caused by the greater shift of people’s activities and transactions on-line during quarantine.

Humana is benefitting from a lower number of visits to physicians, which means lower insurance pay-outs for health care. This trend will most probably return gradually to normal by the end of the year.

The remaining companies are doing roughly as we expected. Some of them are worthy of mention here. Berkshire is unstoppably pressing forward like a mammoth tanker, relying mostly on its insurance, energy and railway segments and large cash reserve. For more about Berkshire, see my recent article “Berkshire Hathaway or S&P 500 Index?”: https://www.vltavafund.com/analyzy/brkindex

I think that every investor who understands the details of Berkshire Hathaway’s business and knows how to value this company must regard its current stock price as a sort of early Christmas present.

Markel is on the one hand expecting higher pay-outs for damages caused by the pandemic (this relates mainly to insurance in the categories for event cancellations and business interruption). On the other hand, it will benefit from rising insurance premiums, which is already visible.

Profits at Sberbank will fall significantly this year. This is probably inevitable for banks during a recession. Despite this, its return on equity at the bottom of the recession will be higher than those of most large western banks in times of expansion. Lockheed Martin and Teekay LNG Partners are practically untouched by the pandemics and recession thus far, and hopefully it will stay that way. By the way, Teekay LNG Partners confirmed during April, in the middle of the greatest quarantine depression, a 31% dividend increase. That is quite an extraordinary step in these times. More frequent in the markets these days are dividend cuts or outright cancellations.

Crest Nicholson had to close down its building sites and sales areas for about two months because of the quarantine. Today, however, they are opened again and activities are gradually returning to normal. Its negative cash flow during this period was quite small. LabCorp’s case is just the opposite from that of Humana. At first, it was hit by a lower numbers of visits to physicians, which brought with it a drop in volume of laboratory tests. This is moving back towards normal now, and the shortfall probably will be more than compensated by a massive increase in Covid testing that already is underway and continues to pick up pace.

Although we are still rather closer to the bottom of the recession than to its end, it seems that our companies have not suffered such serious damages so far and that they will come out of the recession in good condition. If it will appear to us that the situation for any of them is changing, we stand ready to alter our view at any time.

In the quarter just ended, we bought shares of the JP Morgan. In our opinion, among all the world’s large banks, this one is the best managed and financially strongest. It did very well already in the recession of 2008, when it remained profitable and did not require government help. This made it exceptional among large banks, and we may say that this was the year when it stood out most despite the fact that, from the profitability viewpoint, it was the worst year for JP Morgan of the whole previous economic cycle. The worst year of this economic cycle clearly will be 2020. Profits will drop substantially, mainly due to large increase in bad loans. Despite this, JP Morgan should earn a lot of money this year and its strength and quality will again come to the fore. The shares of good banks can be very remunerative long-term “compounders”, and the best time to buy them is usually in times of recession.

We sold Babcock shares. Although we let them go at a low price, we chose to move the money to more aggressive investments into more cyclical companies with greater potential as we near the end of the recession. We lost something on these shares, but fortunately it was a smaller position.

We did much better at Credit Acceptance. We took advantage of the recent favourable prices and we also sold the shares. Our return here was 133% and was also high in absolute terms, as at one time Credit Acceptance was the second largest position in the portfolio after Berkshire Hathaway.

I still owe you the names of stocks we bought at the end of March. These were Humana, Lockheed Martin, Union Pacific and preferred stock of Teekay LNG Partners.

These are very strong and highly profitable companies that have been tested by many a crisis. Lockheed Martin is the world’s biggest company in its industry, and in some parts of its business it is not only dominant but even has a monopoly on the market. Union Pacific has long been in the position of a well-established duopoly, and Humana is a leader in health insurance. The preference shares of Teekay LNG Partners constituted an opportunistic transaction benefitting from dislocation on the ETF market during the March decline. Our investment thesis here has nearly been fulfilled already, but, because the shares still offer a net dividend yield around 9.5%, we may just hold onto them. We have had Humana and Lockheed in our portfolio before, and Union Pacific is here for the first time.

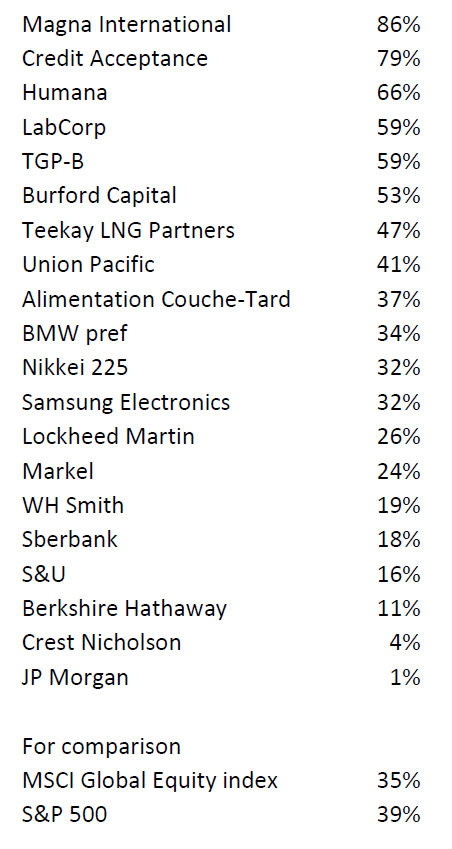

On 23 March, we organised a webinar for you for the first time. It was the only possible form of mass communication, because at that time we all sat closed up in our homes under quarantine. I admit that it was not easy for me to concentrate on webinar preparation and keep a cool head in an environment when a virus was raging across the whole world, economies were closed down, and stock markets were in freefall. Nevertheless, we wanted to analyse in greater detail the individual stocks in the Vltava Fund portfolio with a view to the commencing recession. What none of us anticipated at that time was that later the day of our webinar would prove to be the day when the slump reached its bottom. So that day quite coincidentally provides an interesting baseline for the following table. I’m adding this table for those of you who like numbers better than words, as it shows return on shares in the Vltava Fund portfolio since the day of the webinar, which means from 23 March 2020 through 30 June 2020.

Note: Return on Humana, Union Pacific and Lockheed Martin shares are measured from 24 March 2020 and return on JP Morgan from 20 April 2020, which are the days we first bought them.

The date 23 March 2020 really marked an unexpected turning point. In the evening investors went to bed in the depressed mood that accompanies panic stock sell-offs, and in the morning they woke up to a shopping spree. The main impulse came from the Fed’s announcement that it was initiating massive purchases of various asset types. Very positive effects in the form of money market stabilisation, general provision of liquidity, and a supplying to global markets of too-scarce dollars went hand in hand with the harmful effects of enabling the refinancing of persistently loss-making and highly indebted zombie companies. It was precisely these shares that did best in the subsequent weeks, as they were carried along on an enormous speculative wave pulled by unprecedented activity of retail investors (mainly in the American market) who had time on their hands during quarantine and in large measure cast their government support checks into what in their opinions was the only casino open, that being the stock market.

History teaches us that these fresh-baked “day traders”, who consider the stock market to be a “risk-free money machine”, lose most of their money in the end. I have seen this with my own eyes several times, and therefore it does not trouble us to stand aside from these events. We feel no urge to participate in this risky race with your money, and I think you would not expect that in any case. The speculative mantra of these days is “Fundamentals don´t matter.” Imagine that you went shopping in your supermarket and you were greeted by a large sign “Prices don´t matter.” Would that seem normal to you? I think that prices (and fundamentals) always matter.

The American market is very expensive today. According to S&P, the index´s earnings for the last 12 months are $ 101 per share. With an S&P value of 3100, this means that the market is trading at more than 30 times its profits. At the same time, profits are still falling. For this calendar year, they are expected to be just under $ 92 per share, giving the market a PE of 33.7. It is clear that the market is not traded on the basis of current but expected profits. However, when I imagine how much they would have to increase to match current stock price levels, it does not seem realistic to me in a foreseeable future. Especially if we have higher taxes ahead of Joe Biden´s eventual election victory. These in themselves could reduce corporate earnings by some 10-15%.

Apple, Microsoft, Amazon, Alphabet and Facebook, which account for more than a fifth of the index and are much more expensive than the rest of the market, have the lion´s share of the market recent rise. At the same time, they are far from immune to the ongoing recession, and with the exception of Microsoft, a decline in profits is likely to await them this year. However, they are at least profitable in contrast to another very large group of extremely expensive and mostly chronically loss-making companies, such as Shopify, Wayfair, Uber, Tesla, Nikola, Beyond Meat, Carvana, Okta, Zoom and others. Holding these shares has nothing to do with investing. It is pure gambling and the application of “greater fool theory” in practice. So relying on someone even crazier to buy these shares from me later for an even higher price. At the same time, it is quite likely that some of these companies will not exist in five years.

As soon as this speculative mania passes, it probably will bring in its wake along with large losses for many investors also a collapse of companies due to fraud (such as the recent case of Wirecard), lies, unfinanceable debts (e.g. Hertz), or chronically loss-making business models. The list could be very long, but it will not apply to our investments. Recently, our investments have gone into completely different stocks. Shares of companies whose prices are defensible on the basis of a careful fundamental analysis. You will find them more in the lower floors of the table above. We are not looking for good and conservative investments among companies in which investors euphorically trump each other, who goes further and higher, but among companies that most investors underestimate. There are surprisingly many of them still available and many of them are very cheap. If the prices of some of these shares double over next 2-3 years, they would still not be expensive.

On the whole, however, the sobering up of investors may touch upon the price levels of most stocks, and therefore we have hedged a part of the portfolio using index futures. Moreover, we are holding some proportion in cash at the moment.

Daniel Gladis, July 2020

This article appeared first on ValueWalk Premium.

.fb_iframe_widget_fluid_desktop iframe { width: 100% !important; }

The post Vltava Fund 2Q20 Letter: The Dam Has Broken appeared first on ValueWalk.

Original Article Posted at : https://www.valuewalk.com/2020/07/vltava-fund-2q20-interest-rates-negative/