Spike in Oil Prices Means Good Time to Revamp Budget

Don’t panic over oil prices following the Saudi attack. Make this the right time to revisit your household budget to see where you can cut if fuel prices stay up.

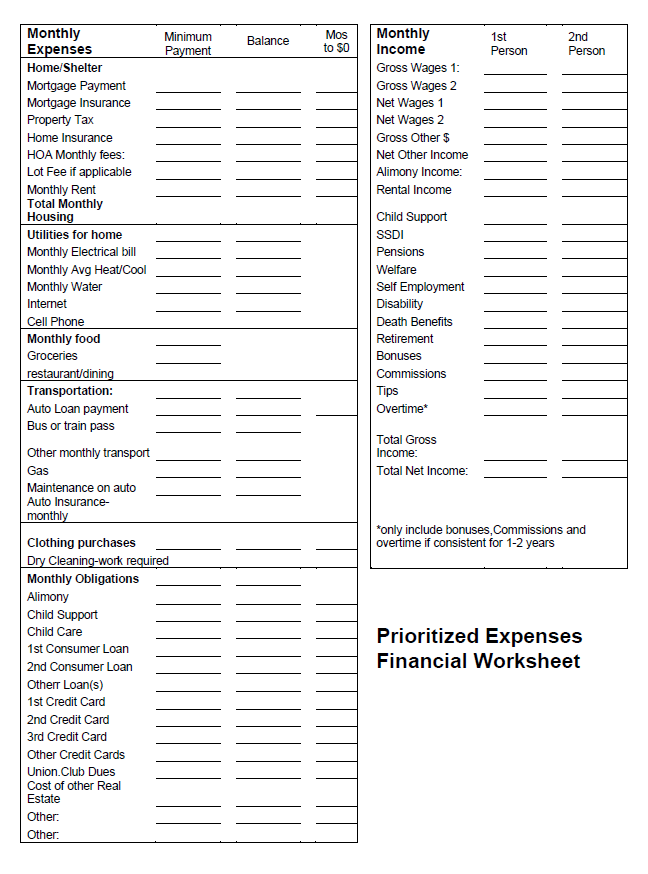

Whether you rent or own, you can complete a simple worksheet to see the amount of your debt and what it would take to pay it off. Think about your monthly obligations in terms of priorities and cost. In those terms, I think of shelter (home), food and clothing and drew up this worksheet based on those needs. After the immediate needs are the other obligations, either caused by emergencies, medical catastrophe or by bad buying decisions. Whatever the cause, you can stop, analyze and make your plan to exit the debt. Want Help? Come see us at DebtFreedomPro.com. If you want to try on your own, come to our site anyway to access helpful hints and tools.

{kind=link}

Fill in the monthly payments and compare to your monthly take home pay for the household. Look over your expenses and figure what accounts can be cut. Then look for high account payments on low balances to see which accounts will fall off soon. Great! You’re making progress.

Hold that thought. Not giving up is the difference between those who reach debt freedom and those who fall off the wagon. Stick to the plan you made, and find free ways to celebrate the accomplishments along the way.

Negotiating reduced settlements. This will close out the account, so only do this if you are willing to lose the buying power, or if the account is already being closed by the creditor. Many creditors will accept less than what is owed on a collection to close it out, but how much less may take longer to negotiate. Try offering half the amount owed and be willing to wait for escalation to get that approved. If you are trying to salvage the account, talk to the creditor and see if you can work out a repayment plan that keeps the account open.