Student Loan Planning: What You Need To Know

As of May 2018, per StudentLoanHero, 75% of graduates from private, non-profit colleges held student loan debt, while 66% of graduates from public non-profit colleges did. As the cost of college continues to rise (well in excess of broader cost-of-living inflation), student loans are often a hotly discussed topic, with planning around them affecting an ever-larger group.

if (typeof jQuery == ‘undefined’) { document.write(”); }

Q1 2020 hedge fund letters, conferences and more

The conversation on college and graduate school funding often evolves around which savings vehicle to contribute to (i.e. 529’s), the tax benefits associated, and withdrawing funds in a way that won’t adversely impact financial aid benefits. However, the other side to this conversation is student loan planning, and the factors to consider when you begin the period where you are now expected to make payments on your loans. Here, we’ll be discussing federal student loans – the types of loans available, repayment plans, and nuances present within.

Types of Loans

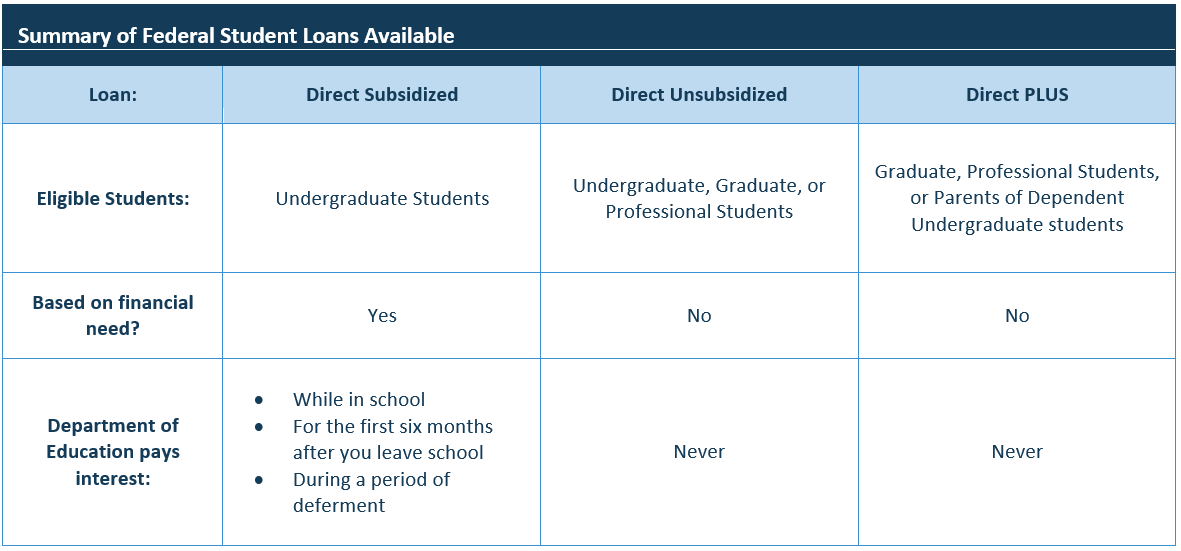

There are four types of student loans available through the U.S. Department of Education’s Federal student loan program:

- Direct Subsidized Loans

- Unsubsidized Loans

- Direct PLUS Loans

- Direct Consolidation Loans

- This is a way of combining various loans into a single loan with a single servicer. As consolidation and potential refinancing of loans likely warrants its own dedicated blog post (stay tuned for this), we’ll\ exclude that from the discussion here.

The distinction in qualifying for Subsidized vs. Unsubsidized Loans is based on financial need – specifically, the difference between the cost of attending the school, and your expected family contribution.

Below is a brief summary of the differences between the types of loans:

As noted above, for subsidized loans, the Department of Education covers interest while the borrower is in school, and for the first six months after leaving school. However, for unsubsidized loans, interest accrual during these periods are ultimately the responsibility of the borrower. What this results in is a “capitalization” of the interest, meaning the interest accrued will be added to the principal amount of your loan. The story does not end here, however. With repayment plans, an additional layer of nuance is added.

Repayment Plans

A host of repayment plans are available to borrowers, with the “Standard Repayment Plan” seeing borrowers pay off their loan in 10 years through fixed payments (akin to an amortizing mortgage). However, this amount may be too burdensome for those just starting out in their careers, which is why there are a number of repayments plans one can choose from (payoff period ranging from 10 to 25 years), including those that cannot exceed a certain percentage of your income (so as to moderate the burden). The following link, taken from The Federal Student Aid office in the DOE, is a helpful resource. It is best to consult with your advisor as you plan to enroll in a specific repayment option.

There is a noticeable amount of uniqueness within each plan, and a number of planning options to consider – for example, for married borrowers, certain repayment plans will look at each borrowers income to determine the percentage to be paid back, whether you file separately or not, whereas others will honor the “separate” filing (MFS). The benefit to this, in certain cases, can be material – by parsing out joint income, the income on which your monthly payments is based upon may be noticeably lower, reducing your monthly payments. However, this must be balanced with any possible additional tax liability from filing separately versus jointly.

Earlier, we touched a bit on interest subsidies, and how they differ for subsidized vs. unsubsidized loans. There’s an additional layer of complexity once you consider the various repayments plans.

Specifically, the following repayment plans are eligible for interest loan subsidies:

- Revised Pay as you Earn (REPAYE)

- Pay as you Earn (PAYE)

- Income-Based Repayment (IBR)

The following article helps explain the differences across each. However, it is important to note that for subsidized loans enrolled in one of the three repayment plans listed above, the government will pay all interest on your subsidized loans for up to three consecutive years. This can be quite helpful, as it’ll work to avoid the capitalization of interest.

Conclusion

Student loan planning can be a very intricate maze to maneuver. However, building a plan for repayment – whether that be the standard 10-year, an income-based repayment plan, or a private refinance, is an important first step.

Wealthspire Advisors is the common brand and trade name used by Sontag Advisory LLC and Wealthspire Advisors, LP, separate registered investment advisers and subsidiary companies of NFP Corp.

Certified Financial Planner Board of Standards, Inc. owns the certification marks CFP®, Certified Financial Planner™ and federally registered CFP (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

This information should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy. The commentary provided is for informational purposes only and should not be relied upon for accounting, legal, or tax advice. While the information is deemed reliable, Wealthspire Advisors cannot guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use. © 2020 Wealthspire Advisors

.fb_iframe_widget_fluid_desktop iframe { width: 100% !important; }

The post Student Loan Planning: What You Need To Know appeared first on ValueWalk.

Original Article Posted at : https://www.valuewalk.com/2020/06/student-loan-planning/